Generals Gathered In Their Masses

YTD Returns as of 3/31/26. Source: Barchart.com. Click for larger image

A large scale attack on Iran sent oil prices soaring and world equity markets tumbling in March as frozen traffic in the Strait of Hormuz sparked what many are calling the largest oil supply shock in history.

With crude oil prices nearing $120 a barrel, inflation worries sent global interest rates sharply higher, complicating the outlook for Fed rate cuts in 2026 and threatening to put further strain on an already troubled private credit sector that saw several funds limit client withdrawals during the month.

Given the headlines, stock markets were remarkably composed with 20-day realized volatility in the S&P 500 barely reaching the mid-teens despite a 5% drop in March while a comparatively large jump in VIX hinted at a "hedge and hold" mentality, presumably in anticipation of an imminent off ramp in the Iran conflict. While this turned out to be a fairly good template for last year's tariff standoffs, the situation in Iran is complicated by an oil price shock that embeds itself deeper into the system every day that the mess is not contained.

Despite a sharp bounce for stocks on the 31st that reversed a sizeable portion of the March gains in VIX futures, TCM strategies saw modest hedging gains on the month with Risk Managed Equities portfolios performing largely in line with traditionally-hedged equity peers in March and on the year.

LET THEM EAT CAKE

Beyond simply reducing volatility, TCM risk management pursues a risk-reward balance that seeks to minimize costly emotional errors. This balance is critical because both extremes are equally dangerous: while an overly aggressive portfolio is bound to trigger the primal 'fear of losing money,' an overly conservative one often breeds the more subtle, yet equally destructive, 'fear of missing out.'

Practically speaking: too much volatility makes a strategy hard to endure, while insulating all drawdowns sacrifices market-level returns. By targeting the 'sweet spot' in the middle, TCM strategies seek to let investors have their cake and eat it too— equity-like returns with genuine crisis risk management.

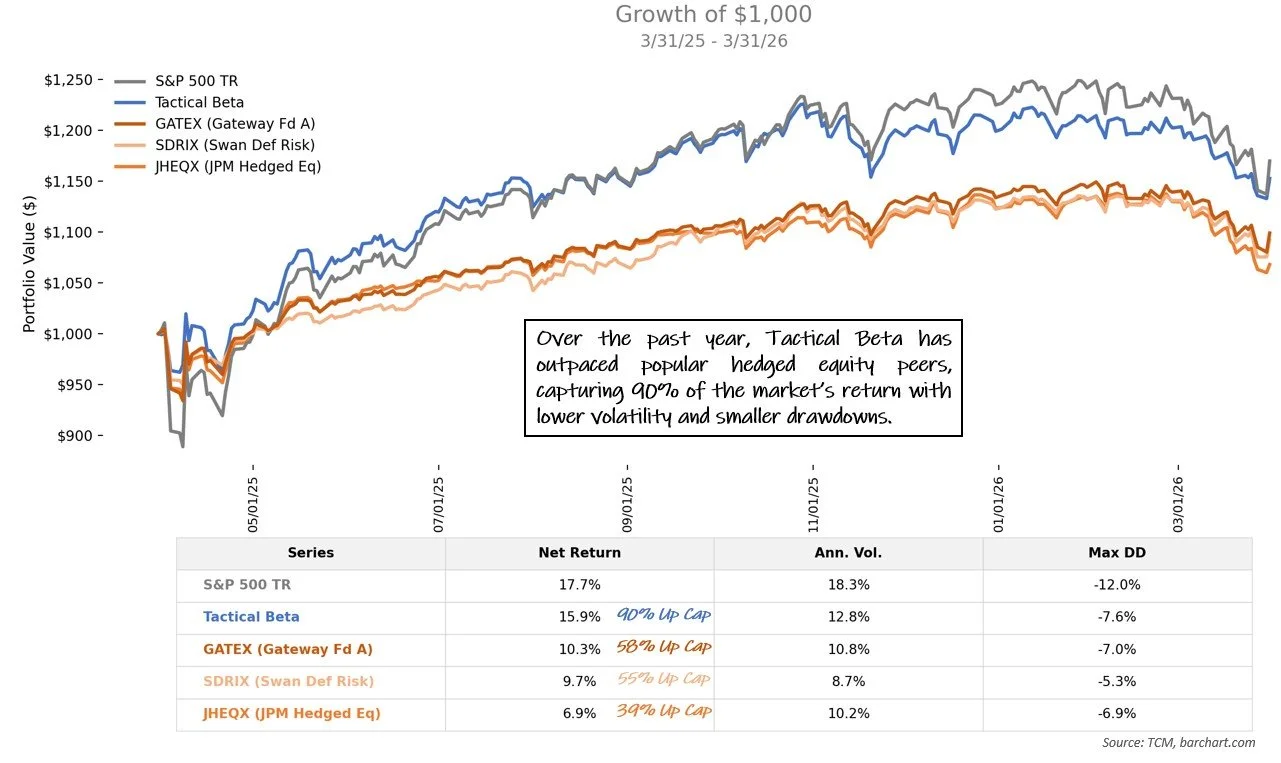

The longest running Risk Managed Equity strategy at TCM, Tactical Beta has often achieved this feat over its nearly 10 year history. In the latest example, the strategy has captured 90% of the S&P 500’s return over the past 12 months with lower volatility and smaller drawdowns, much closer to the “sweet spot” than popular hedged equity peers* that are often hindered by continuous hedging (chart).

Rolling 1y net performance as of 3/31/26. Source: TCM, barchart.com. Click for larger image

Far from a fluke, a similar story can be told over the past two years, three years and since inception, with hedged equity peers keeping pace only during the five-year lookback period that currently starts on the cusp of Tactical Beta’s least favorable environment, a rare low volatility bear market in the S&P 500.

While the Iran confrontation may have eased, investors still face AI-driven disruption rippling through private credit, November's midterms, and how these forces interact with interest rates in a fragile economy. We don't know what's ahead, but we do know our process handles uncertainty well.

*JP Morgan Hedged Equity (JHEQX), Swan Defined Risk (SDRIX) and Gateway Fund A (GATEX)