Introducing the Vol Dash by TCM, a weekly update on markets and positioning through the lens of TCM’s Volatility Dashboard.

Vol Dash for week ended 6/26/26

While “Mag 7” weakness weighed on the S&P 500 last week, strength beneath the surface pushed smaller and broader indexes — including the Russell 2000 and equal-weight S&P 500 — toward record highs. Rather than signaling a retreat from risk assets, the price action looked more like a rotation within equities.

MTD Returns as of 6/26/26. Source: barchart.com. Click for larger image

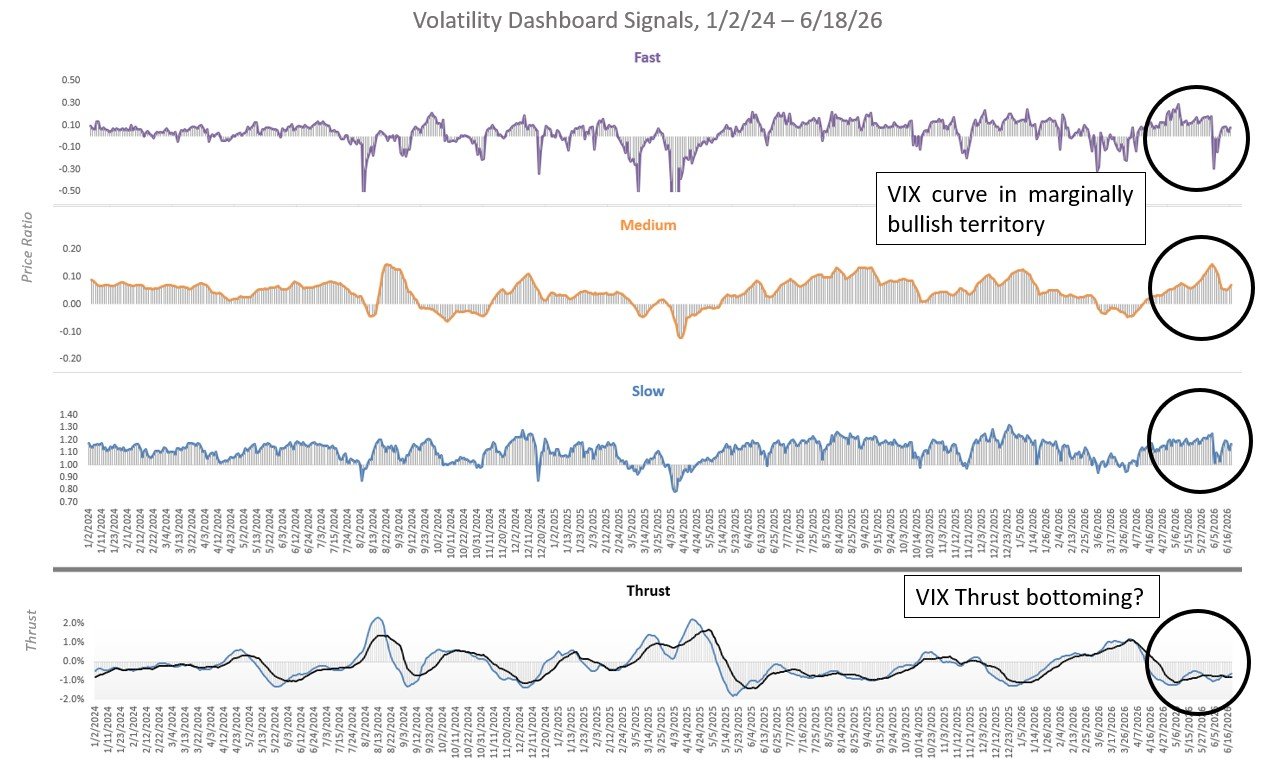

As is often the case, this type of sector rotation has so far produced only marginal changes in pricing for VIX contracts, which remain more closely tied to index-level volatility than dispersion beneath the surface. With stocks entering a seasonally constructive period, the coming holiday-shortened week could provide another test of market breadth, particularly with Thursday’s jobs report serving as the key macro catalyst.

TCM Volatility Dashboard Signals 1/2/24 - 6/26/26. Source: TCM. Click for larger image

Exposure Update for week ended 6/26/26

Tactical Beta and Tactical Q closed index hedges early last week, looking to increase exposure if VIX signals improve.

Tactical Beta daily exposure, trailing 100 day as of 6/26/26. Source: TCM. Click for larger image

Tactical Q daily exposure, trailing 100 day as of 6/26/26. Source: TCM. Click for larger image