A Material World

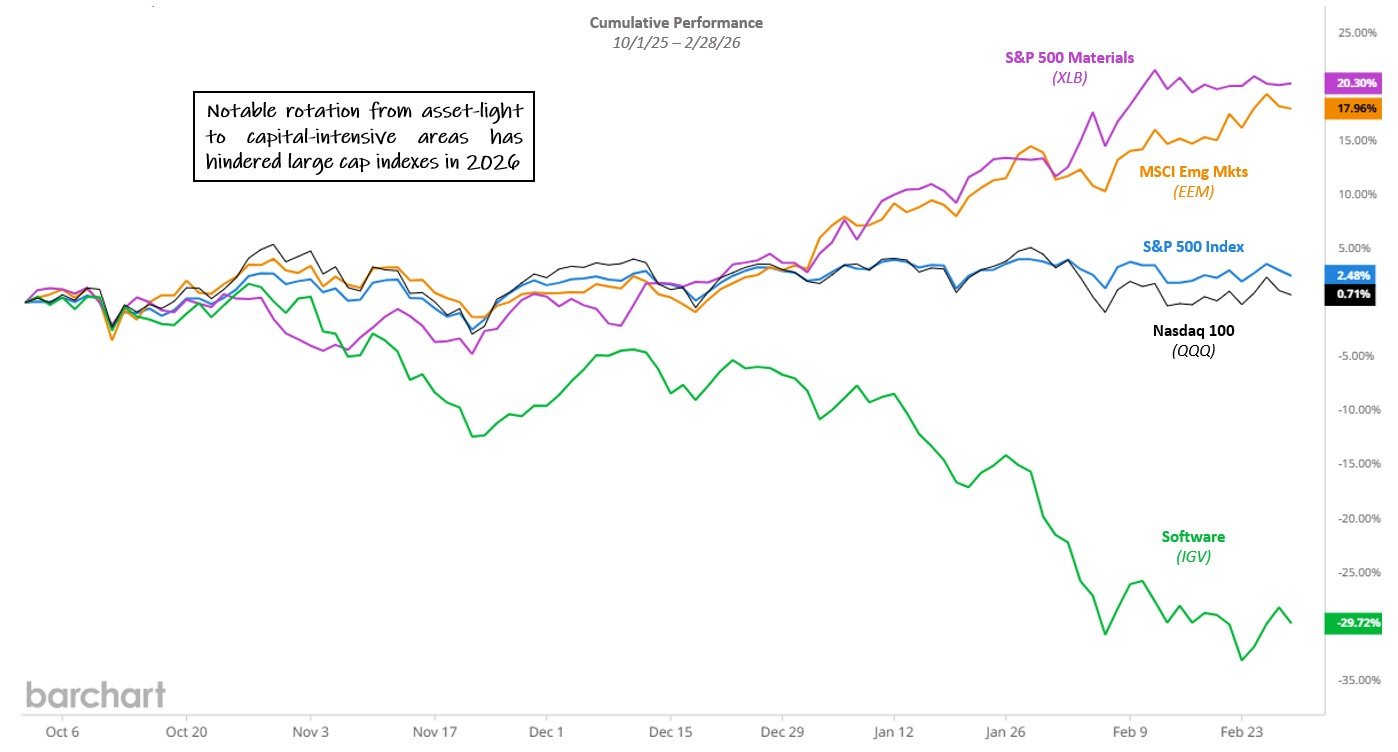

A shift from asset‑light tech to capital‑intensive “make‑stuff” sectors and regions (chart) kept the S&P 500 index stalled just below all-time highs in February with significant sector dispersion keeping overall market volatility relatively subdued. In what has become a common refrain in 2026, this rotation once again benefitted ex-US markets that have greater industrial exposure than their US counterparts, in particular the MSCI Emerging Markets Index which has already gained 14.8% on the year through February.

Cumulative Performance 10/1/25 - 2/28/26. Source: barchart.com. Click for larger image

Despite a tricky environment in which VIX Dashboard signals remained on edge though short of crisis territory, TCM strategies managed modest hedging profits on the month with all Risk Managed Equities strategies ahead of their benchmarks in February. While TCM’s philosophy and the math of compounding argue that only crisis drawdowns are worth the cost of mitigation, small relative wins can also be helpful provided there is a process to realize them consistently. Much easier said than done, TCM continues to refine methods to do so.

Somewhere Between Heaven and Hell

As “AI replacement” fears jump from software to logistics to brokerages, the market seems to be convinced of the massive productivity gains of AI on the one hand, while simultaneously fearing losses on the investments into the same technology- a paradox that reflects the massive uncertainty around AI which could either be the end of scarcity, the end of humanity, or somewhere in between (chart).

With Walmart now trading at a higher P/E than Amazon and Coke higher than Microsoft, the market seems to be heavily discounting Mag 7 prospects (chart) that were widely touted just a few months ago, opening a substantial gap with fundamentals that may be storing up future market volatility, either positive or negative.

Nvidia (NVDA) Price vs Fwd EPS Estimates, Dec 2022 - Feb 2026. Source: Goldman Sachs. Click for larger image

Based on historical precedent, what’s certain is that there will be bumps along the road and whenever there is significant debt involved, miscalculations can quickly spiral into a market crisis scenario of cascading defaults and loss of confidence. Given the range of current predictions for AI, we believe investors would be especially well-advised to either keep their crystal ball polished or include a risk-aware element in their portfolios.