TUG OF WAR

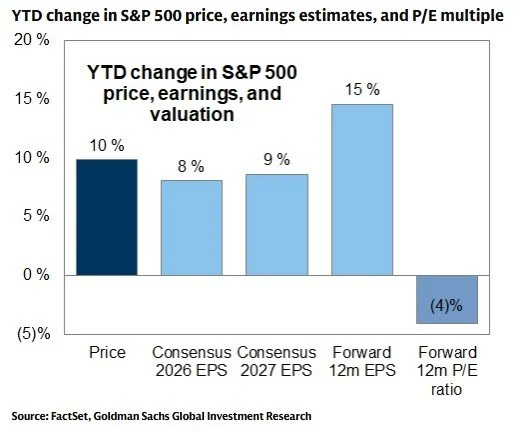

Despite a healthy YTD gain, the forward P/E multiple for the S&P 500 has declined in 2026. Source: Goldman Sachs. Click for larger image.

In a tug-of-war between AI optimism and macro/geopolitical stress, US equities (Nasdaq 100 +10.5%, S&P 500 +5.3%) pushed to fresh records in May as strong technology earnings and renewed enthusiasm for AI infrastructure spending outweighed risks from high oil prices and elevated bond yields.

Thanks to light hedge exposure signaled by the Vol Dashboard, TCM Risk Managed Indexing strategies once again captured the lion’s share of May’s rally, with Tactical Beta easily outpacing the hedged equity peers composite* in May, extending its lead over these industry stalwarts in 2026 as well as in each of the rolling 1, 2, 3, 5 and since inception periods. Benefitting from more direct exposure to AI and related themes, Legacy Navigator (+5.8% May) and Hedged Disruptor (+13.7% May) also saw solid gains on the month.

Clearly the market’s central bullish force, the AI-powered rally so far appears justified by fundamentals. In fact, with forward earnings estimates outpacing the market’s rise in 2026, forward valuation multiples for the S&P 500 have actually declined since the start of the year despite a healthy +11% YTD gain for the index (chart). While estimates can certainly change, for now they have given the bulls a place to hang their hat.

*Equal weighted composite of JPM Hedged Eq (JHEQX), Swan Def Risk (SDRIX) and Gateway Fd A (GATEX), rebalanced monthly

Dire Straits

In the background, Iran remains an obvious risk with elevated oil prices and disruptions in the Strait of Hormuz (chart) raising fears of another inflation shock that could significantly complicate the Fed’s easing plans. Indeed, the April FOMC minutes, released in May, noted that inflation remained elevated and had moved higher, led by energy prices. That kept investors focused less on near-term rate cuts and more on whether the Fed might have to stay restrictive—or even tighten—if the oil shock persisted.

Strait of Hormuz tanker volume, 1 year as of 5/24/26. Source: Goldman Sachs. Click for larger image

Perhaps most concerningly, bond markets have become extremely volatile as high energy prices, sticky inflation, fiscal deficits, and reduced prospects for Fed cuts threaten to keep rates higher for longer. In May, the U.S. 30-year Treasury yield briefly moved above 5.2%, its highest level since 2007, before rate volatility eased as oil prices fell and peace-deal hopes improved (chart).

MOVE Index vs VIX Index, 1 year as of 5/28/26. Source: Goldman Sachs

Since they tend to move slowly, timing the impact of macro issues like inflation or sovereign debt is notoriously difficult. While it is easy to identify potential sparks for the next market crisis, insuring against them profitably is quite another matter, and one that we believe is best addressed with a consistent tactical process.