Introducing the Vol Dash by TCM, a weekly update on markets and positioning through the lens of TCM’s Volatility Dashboard.

Vol Dash for week ended 6/5/26

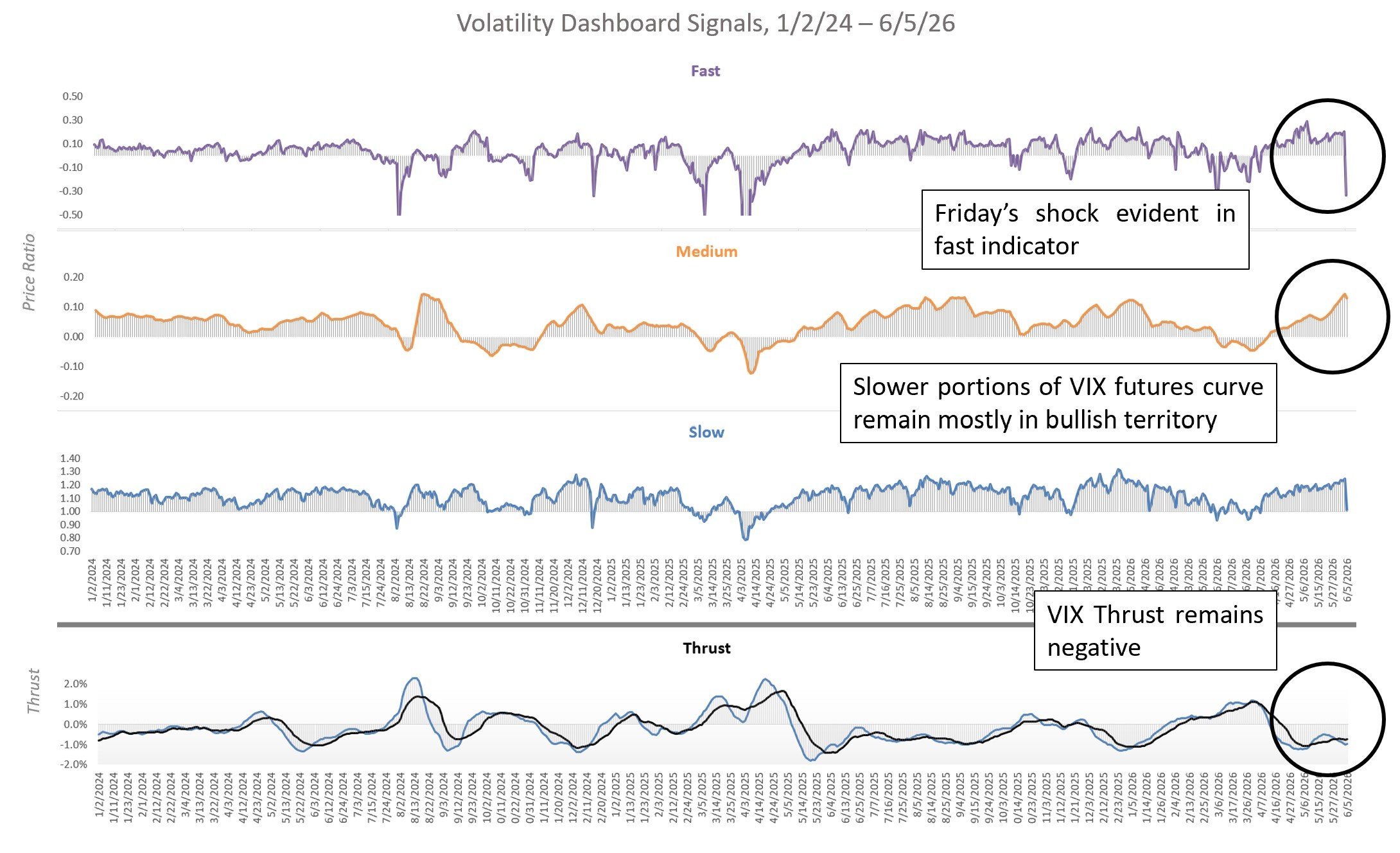

Sparked rising interest rates following Friday's hotter than expected payrolls report, last week ended with a liquidation centered on AI-related names that have seen a substantial rally from the March lows.

While stress was clearly evident in the most reactive parts of the VIX futures curve, Friday's equity selloff was not accompanied by any risk-off widening in corporate credit spreads, bolstering its case as a one-off equity event. In this context, this week's CPI report will carry extra importance for its potential impact on interest rates.

TCM Volatility Dashboard Signals 1/2/24 - 6/5/26. Source: TCM. Click for larger image

Exposure Update for week ended 6/5/26

In the typical approach to "clear air turbulence" which tends to see quick mean reversion in VIX, Tactical Beta and Tactical Q held off on adding VIX exposure into Friday's spike, with any new VIX positions pending this week's market response.

Tactical Beta daily exposure, trailing 100 day as of 6/5/26. Source: TCM. Click for larger image

Tactical Q daily exposure, trailing 100 day as of 6/5/26. Source: TCM. Click for larger image